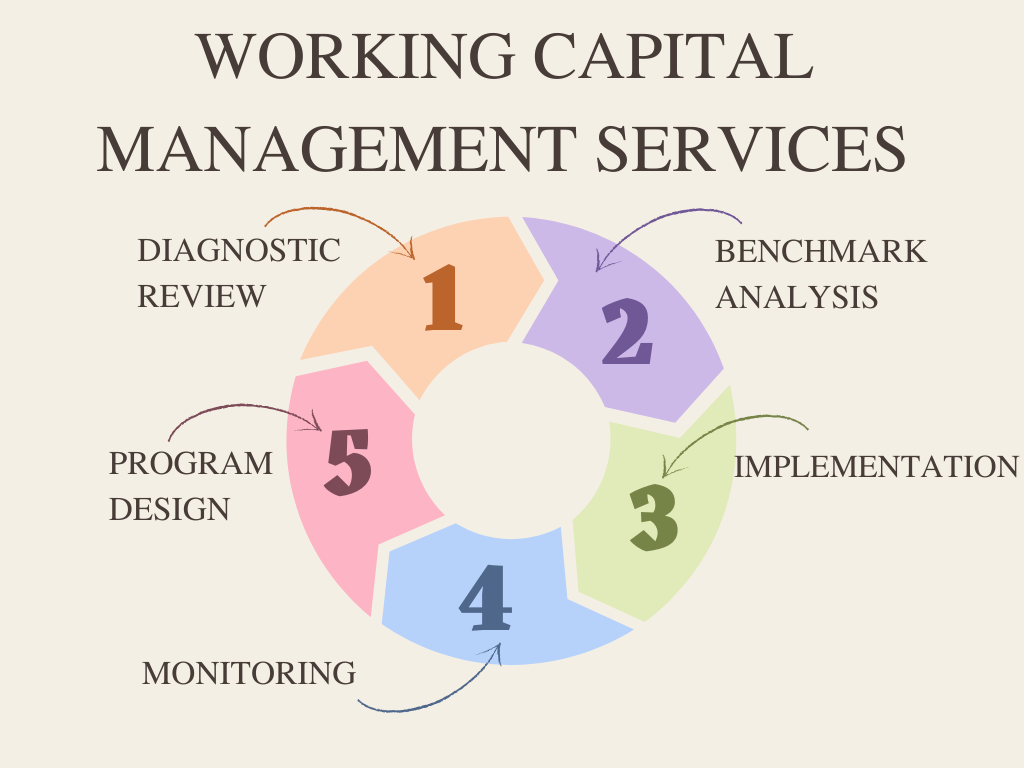

Treasury Management

Treasury management is the management of enterprise holding. It is a key component of business operations. In the business landscape. The importance of treasury management cannot be denied...

Tips For Managing Business Through Finance

All successful businesses have a strong finance function, and that differentiates the best from the others. Here are quick tips for managing the business through...

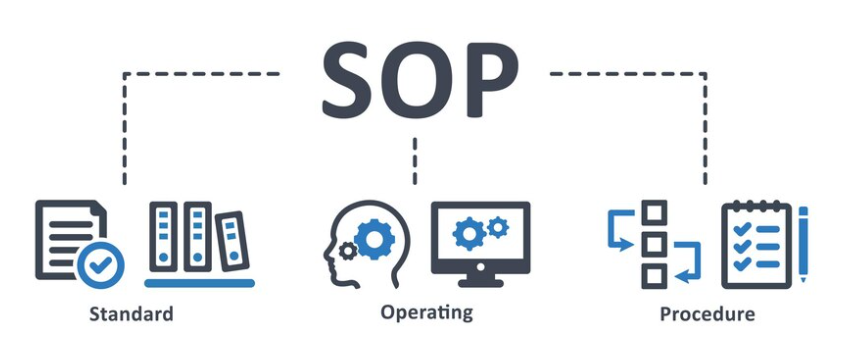

Standard Operating Procedures (SOPs)

A Standard Operating Procedure (SOP) is a set of written instructions that describes activities necessary to complete the task under industry regulations. An SOP is a document containing step-by-step instructions..

Business Process Re-engineering

BPR stands for Business Process Re-engineering. Business process reengineering is a management strategy and a systematic approach to improve product quality and reduce organizational cost, service, and speed...